Rabu, 03 Juli 2019

Under pressure from Trump, OPEC embraces Putin - The Globe and Mail

/arc-anglerfish-tgam-prod-tgam.s3.amazonaws.com/public/TREEYBR6RNHDRCWCBZQYYRD7WQ.JPG)

When Vladimir Putin announced at the weekend that OPEC would extend oil production cuts, broadcasting a deal before the group had even met to approve it, the move angered some member nations.

They were dismayed at the leading role non-OPEC Russia, once seen as an enemy in oil markets, was playing in shaping the group’s policies.

But reality soon set in, and the acceptance that Moscow could help OPEC in its goal of propping up oil prices at a time when it is facing intensifying heat on another front: from U.S. President Donald Trump.

Trump is putting unprecedented pressure on OPEC and its de-facto leader Saudi Arabia, demanding they pump more crude to drive down fuel prices - a key domestic issue for him as he seeks re-election next year.

Iranian Oil Minister Bijan Zanganeh initially expressed outrage about Russian President Putin’s pre-announcement of the extended output cuts.

“OPEC is going to die with these processes,” he declared on Monday morning, before OPEC oil ministers met to effectively rubber-stamp a done deal, bemoaning the Russia-Saudi dominance of the group’s affairs.

But by Monday evening, he had thrown his support behind the deal: “The meeting was good for Iran and we achieved what we wanted.”

OPEC and Russia have become unlikely bedfellows, forging an “OPEC+” alliance to reduce global crude supply to counter soaring output from the United States and a weakening world economy.

It is a marriage of convenience as both want higher oil prices to shore up their finances, while the alliance could also strengthen OPEC’s position in the face of Trump’s demands.

“I don’t think Russia is calling the shots,” said Saudi Energy Minister Khalid al-Falih when asked if Putin was now OPEC’s boss. “I think Russia’s influence is welcome.”

Iran’s veteran OPEC governor Hossein Kazempour Ardebili concurred, echoing his boss Zanganeh’s conciliatory tone.

“Russia is a big player. If it announced something in agreement with the rest of OPEC, this is most welcome,” he said. “We are working together.”

Iraq, which has overtaken Iran as OPEC’s second-largest producer after Saudi Arabia and has taken its market share in Europe and Asia, also said Moscow’s rising role was positive.

Such a chorus of approval is a sharp reversal for relations between OPEC and Russia that have been characterised by antipathy and distrust for decades.

Back in 2001, Russia agreed to cut production in tandem with OPEC but never delivered on its pledges and instead raised output. That severely damaged relations, and other attempts at cooperation were unsuccessful - until the recent alliance.

In his book “Out of the Desert”, former Saudi Oil Minister Ali al Naimi wrote that his 2014 meeting with Russian officials lasted just minutes. Upon learning Russia would not cut output, he gathered his papers and said: “I think the meeting is over.”

CHANGING DYNAMICS

Putin announced on Saturday that he had met Saudi Crown Prince Mohammed bin Salman on the sidelines of a G20 meeting in Osaka and they had agreed to extend the OPEC+ production cuts.

Gary Ross, chief executive of Black Gold Investors, said that even if it was “indelicate” for Saudi Arabia to let Putin announce the deal, it showed the changing oil market dynamics.

“Trump has one interest – low oil prices. Putin wants higher prices,” said Ross, a veteran OPEC watcher. “Putin is vitally important for OPEC. And it is still in Russia’s best interest to cooperate with OPEC as half its budget comes from energy revenues.”

Russia needs prices of $45-50 a barrel to balance its budget and its finances are stretched by U.S. sanctions imposed following its annexation of Crimea. Saudi Arabia needs an even higher price of $80. Benchmark Brent crude is currently in the region of $65 a barrel.

But just as the collaboration could lend Saudi Arabia some support against Trump, who has demanded Riyadh increase oil supply if it wants U.S. military support in its standoff with regional rival Iran, it also gives Putin more than extra revenues.

Good relations with Riyadh, an American ally, bolsters Moscow’s clout in the Middle East, helps Putin’s campaign in Syria and might even help mend relations with Washington, according to two sources in Russia’s delegation to Vienna, where OPEC officials have been meeting.

Highlighting those intersecting roles, Russian Energy Minister Alexander Novak also serves as head of several Russian government commissions on trade and cooperation including with Saudi Arabia, Iran, Turkey and Qatar.

Iran’s change in tone, in particular, illustrates the conflicting political and economic pressures it faces.

Tehran’s falling production, due to U.S. sanctions reimposed and extended by Trump, has reduced its role within OPEC while increasing those of Saudi Arabia and non-OPEC Russia.

Iran’s exports plummeted to 0.3 million barrels per day in June from as much as 2.5 million bpd in April 2018. Oil output in OPEC’s exempt nations: https://tmsnrt.rs/2Fx7Lcc

But Iran is itself also looking to help from Russia, one of just a few countries that has offered to aid Tehran to counter the sanctions choking its oil trade and hammering its economy.

Two Russian energy industry sources said some work was being done to boost the Iranian economy but talks were slow and difficult, without giving details of the nature of the plans.

from Business - Latest - Google News https://ift.tt/2ROMcsO

via IFTTT

July 03, 2019 at 01:09PM

Lagarde to succeed Draghi as ECB chief amid weakening economy - BNNBloomberg.ca

Christine Lagarde is set to swap the helm of the International Monetary Fund for that of the European Central Bank, becoming the first woman to run euro-area monetary policy just as the bloc’s economy looks in need of fresh stimulus.

Lagarde was nominated to succeed Mario Draghi as president of the ECB when his eight-year term ends on Oct. 31. European leaders turned to the 63-year old onetime lawyer and former French finance minister on Tuesday after hours of negotiations in Brussels over a package of top EU jobs.

In a statement, Lagarde said that she was “honored to have been nominated” and would temporarily relinquish her responsibilities at the IMF while EU lawmakers look to ratify her appointment.

“She was chosen because she took on an indisputable leadership role at the IMF and I think whoever can do that can also lead the ECB,” German Chancellor Angela Merkel said. French President Emmanuel Macron said “she has the qualities and competence for the ECB. She has credibility with the markets.”

In moving from Washington to Frankfurt, Lagarde will be tasked with driving monetary policy in a 19-nation economy which Draghi has already signaled will need more help, likely in the form of lower interest rates and possibly with the resumption of quantitative easing. Inflation is running at barely half the ECB’s goal of just under 2 per cent despite years of negative rates and 2.6 trillion euros (US$3 trillion) of bond purchases.

Investors will likely bet that as a seasoned crisis-fighter, Lagarde will share Draghi’s taste for aggressive and innovative monetary policy, especially as her appointment means the more hawkish Bundesbank President Jens Weidmann misses out.

Financial markets are already pricing an ECB rate cut by September, in line with predictions by ECB watchers at Bloomberg Economics and Goldman Sachs Group Inc. Morgan Stanley said the choice of Lagarde increases their “conviction” that the ECB will eventually resume buying bonds.

Moliere’s Trees

Lagarde last week described the world economy as hitting a “rough patch” and advised central banks to continue to adjust their policies in response. In June 2014, she said she would “certainly hope” the ECB would conduct QE if inflation stayed sluggish -- months before it announced it would do so.

She also praised Draghi’s 2012 commitment to do “whatever it takes” to save the euro and recently echoed his call for governments to do more to battle future downturns. In March, she linked the need to fortify the euro area to the words of playwright Moliere: “The trees that are slow to grow bear the best fruit.”

What Bloomberg’s Economists Say

“The ECB will be a different central bank under Lagarde than it has been under Draghi, but the absence of a Ph.D. may not matter. Draghi’s skills lay as much in navigating European politics as in formulating policy. If the new central bank president has just one skill, it’s the former.”

-- Jamie Murray. See his ECB INSIGHT

Just last September, Lagarde dismissed speculation she could take over the ECB, telling the Financial Times she was a “ bit annoyed and fed up” with the suggestion. Only one economist surveyed last month predicted she would get the job, with Weidmann seen as the most likely winner in a race dominated by men.

France has now twice secured the presidency of the two-decade-old ECB. Draghi, an Italian, was preceded by Frenchman Jean-Claude Trichet, who replaced Dutchman Wim Duisenberg.

In common with Trichet, whose appointment was held up by a trial involving the bailout of Credit Lyonnais, Lagarde brings a history of legal wrangles. They culminated in a conviction of negligence in 2016 over her handling of a multi-million euro dispute linked to the same bank.

Lagarde’s appointment also means the ECB and the U.S. Federal Reserve will be headed by former lawyers, a shift from the era when central banks were run by academic economists such as Ben Bernanke. That opens her up to criticism that she lacks the knowledge to set monetary policy and could boost the influence of Philip Lane, the ECB’s new chief economist.

“It is a little puzzling because she’s not known as one of the leading economic minds out there,” said Alicia Levine, chief strategist at BNY Mellon Investment.

She does though boast political nous, which will be needed to unite fellow ECB officials when setting policy -- especially if they run low on monetary ammunition and need to nudge governments to step up support of the economy.

“She has the political skills needed to build consensus on the Governing Council, is a good communicator and has the standing and backbone to defend the ECB’s decisions on the larger European stage,” said Krishna Guha, head of central bank strategy at Evercore ISI. “She would be forceful in calling on member states to make use of the fiscal space.”

EU Council President Donald Tusk dismissed concerns about Lagarde’s lack of formal economic training. She will make a “perfect” ECB president, he said in Brussels.

Alongside Sabine Lautenschlaeger, Lagarde will be one of two women on the six-member Executive Board. They are likely to be the only two female participants in the 25-member Governing Council, which includes the governors of euro-region national central banks and has long been dominated by men.

Broader View

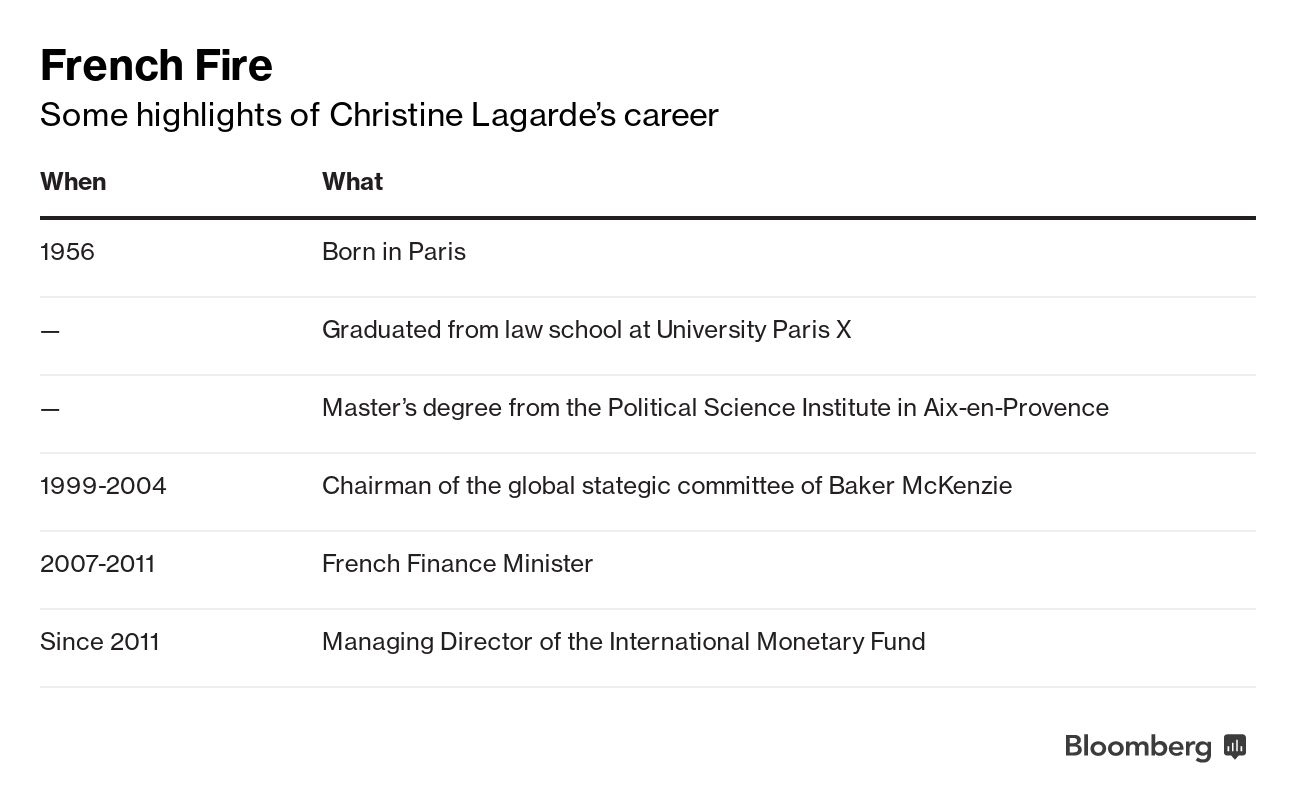

Lagarde was also the first woman to serve as managing director of the IMF, being first appointed in 2011 and then handed another five year term in 2016. Her exit will likely spark a fight between capitals over whether a European should always run the lender or if it’s time for an emerging-market candidate to do so.

At the IMF, Lagarde helped negotiate the fund’s biggest ever bailout when it handed more aid last year to Argentina. She also sought to give emerging economies such as China more of a voice in its management, while putting greater emphasis on issues including climate change and income and gender inequality. That helped broaden the fund’s image beyond its reputation as an advocate of budget cuts.

She sometimes clashed with countries whose monetary policy she will now help set. As the leader of one of Greece’s major creditors, she found herself both pressuring the country to accept austerity to keep it in the euro-zone while at the same time persuading its European partners to allow debt relief. In 2018, she and Weidmann disagreed publicly after she called upon Germany’s government to spend more and close its current account surplus.

Lagarde was educated in France and the U.S., working as an intern in the U.S. Congress for a time. On graduating from the University of Paris, Nanterre, she joined the Paris office of Chicago-based law firm Baker & McKenzie LLP. She focused on employment law and mergers and acquisitions, rising through its ranks to become a partner in 1987 and then its chairman in 1999.

Then-French President Jacques Chirac launched her political career in 2005 by appointing her minister for trade. She went on to serve as minister for agriculture before becoming the first woman to become finance minister in a Group of Seven economy in June 2007.

She held that role as the collapse of Lehman Brothers Holdings Inc. set off a global recession and paved the way for the euro-area debt crisis. During the all-night talks of policy makers that followed she often sought to boost morale by passing M&M’s chocolates around fellow finance chiefs.

“If it had been Lehman Sisters rather than Lehman Brothers, the world might well look a lot different today,” she once said.

A past member of France’s synchronized swimming team, Lagarde said her experience in the pool had taught her how to “grit your teeth and smile.”

from Business - Latest - Google News https://ift.tt/2ROMFLB

via IFTTT

July 03, 2019 at 12:39AM

Job creation has another rough month in June as private payrolls rise by just 102,000 - CNBC

Tara Skipper, talent acquisition partner talks to persecutive job applicants at the USC booth during the Veterans Employment Fair held at the Carson Civic Center in Carson on Wednesday, June 26, 2019.

Brittany Murray | Getty Images

Job creation looks to have had another rough month in June, with private companies adding just 102,000 new positions, according to a report Wednesday from ADP and Moody's Analytics.

That missed even the meager 135,000 estimate from economists surveyed by Dow Jones and comes off the weak May growth of just 41,000. The May number was revised up from an initially reported 27,000.

The disappointment sets the stage for another possible letdown from the more widely watched nonfarm payrolls report from the Labor Department, which will be released Friday and is expected to show growth of 165,000 after May's lackluster 75,000.

"The economy's growth rate is significantly slowing, and I think the risks are rising that it's going to stall out," Mark Zandi, chief economist at Moody's Analytics, told CNBC. "I think the economy is on the razor's edge, and this number is consistent with that view."

Economic data overall has been wobbly lately as economists see growth slowing in 2019 and a possible recession ahead in 2020.

"The job market continues to throttle back," Zandi said in a statement. "Job growth has slowed sharply in recent months, as businesses have turned more cautious in their hiring. Small businesses are the most nervous, especially in the construction sector and at bricks-and-mortar retailers."

Small companies take a hit

Indeed, companies with fewer than 50,000 employees saw another setback in June, with payrolls falling by 23,000 after a decline of 52,000 the previous month. Businesses with fewer than 20 employees were particularly hard-hit, subtracting 37,000 jobs.

On the upside, job creation was fairly strong among bigger businesses. Companies with 50 to 499 employees posted growth of 60,000, while large businesses added 65,000.

At the industry level, goods producers on net lost 15,000 jobs. Construction fell by 18,000 while natural resources and mining lost 4,000. Manufacturing added 7,000.

Service-related industries provided all the job growth, adding 117,000 positions. Education and health services led the way with 55,000 and professional and business services contributed 32,000 to the total. Trade, transportation and utilities added 23,000 though leisure and hospitality rose by just 3,000 after adding 16,000 in May. Franchises grew by 13,500.

"While large businesses continue to do well, small businesses are struggling as they compete with the ongoing tight labor market," added Ahu Yildirmaz, vice president and co-head of the ADP Research Institute. "The goods producing sector continues to show weakness. Among services, leisure and hospitality's weakness could be a reflection of consumer confidence."

The Conference Board's measure of consumer sentiment in June fell to its lowest level in nearly two years as worries intensify over tariffs and expectations dim for job growth.

Despite the slowdown in hiring, there remain 1.6 million more jobs than workers counted among the unemployed, a record high. The tight labor market has produced only a modest boost in wages, however.

As worries over the economy grow, markets are expecting a policy response from the Federal Reserve. Wall Street expects the central bank to cut interest rates at its meeting later this month, though Fed officials remain mostly noncommittal.

https://www.cnbc.com/2019/07/03/adpmoodys-private-payrolls-rise-102000-in-june-vs-135000-est.html

2019-07-03 12:15:45Z

CAIiEI-ydJHeO0VEHmg7BkquX3kqGQgEKhAIACoHCAow2Nb3CjDivdcCMJ_d7gU

Canopy Growth Corporation Co-CEO Bruce Linton to step down - Yahoo Finance

Canadian cannabis company Canopy Growth Corporation (CGC, WEED.TO) unexpectedly announced Wednesday that Bruce Linton would be stepping down as co-chief executive officer and board member of the firm.

Mark Zekulin, currently president and co-chief executive officer, will remain on as CEO of Canopy, the world’s largest publicly traded cannabis company by market capitalization. Zekulin will work with the board of directors to identify a new leader for the company in a search that will include both internal and external candidates, Canopy said in the statement.

Rade Kovacevic, current head of Canadian operations and recreational strategy, will fill the role as president. Each of the executive changes are effective immediately.

"The Board decided today, and I agreed, my turn is over. Mark has been my partner since this Company began and has played an integral role in Canopy's success,” Linton said in a statement. “While change is never easy, I have full confidence in the team at Canopy – from Mark and Rade's leadership to the full suite of leadership – as we progress through this transition and into the future."

Shares of Canopy fell 7% to $37.24 each as of 7:49 a.m. ET on the New York Stock Exchange.

Linton, a co-founder of Canopy, had been a leader at the company since its inception in 2013, when it was first known as Tweed Marijuana. Canopy became the first publicly traded cannabis company in North America in April 2014.

In 2018, Canopy received a $4 billion investment from Corona-owner Constellation Brands (STZ), giving the beverage-maker an about 40% stake in the company. Constellation Brands’ CEO Bill Newlands and CFO David Klein serve as members of Canopy’s board of directors.

“We fully support the decision made by Canopy Growth’s Board of Directors to appoint Mark Zekulin as the company’s sole CEO,” a spokesperson from Constellation Brands said in a statement to Yahoo Finance. “The future of Canopy Growth remains very bright and we look forward to the company’s continued success for many years to come.”

For the fiscal year ending in March, Canopy brought in net revenue of $226.3 million, while its adjusted EBITDA amounted to an annual loss of $257.0 million.

This post is breaking. Check back for updates.

https://finance.yahoo.com/news/canopy-growth-corporation-co-ceo-bruce-linton-steps-down-112230140.html

2019-07-03 11:22:00Z

CBMiZmh0dHBzOi8vZmluYW5jZS55YWhvby5jb20vbmV3cy9jYW5vcHktZ3Jvd3RoLWNvcnBvcmF0aW9uLWNvLWNlby1icnVjZS1saW50b24tc3RlcHMtZG93bi0xMTIyMzAxNDAuaHRtbNIBAA