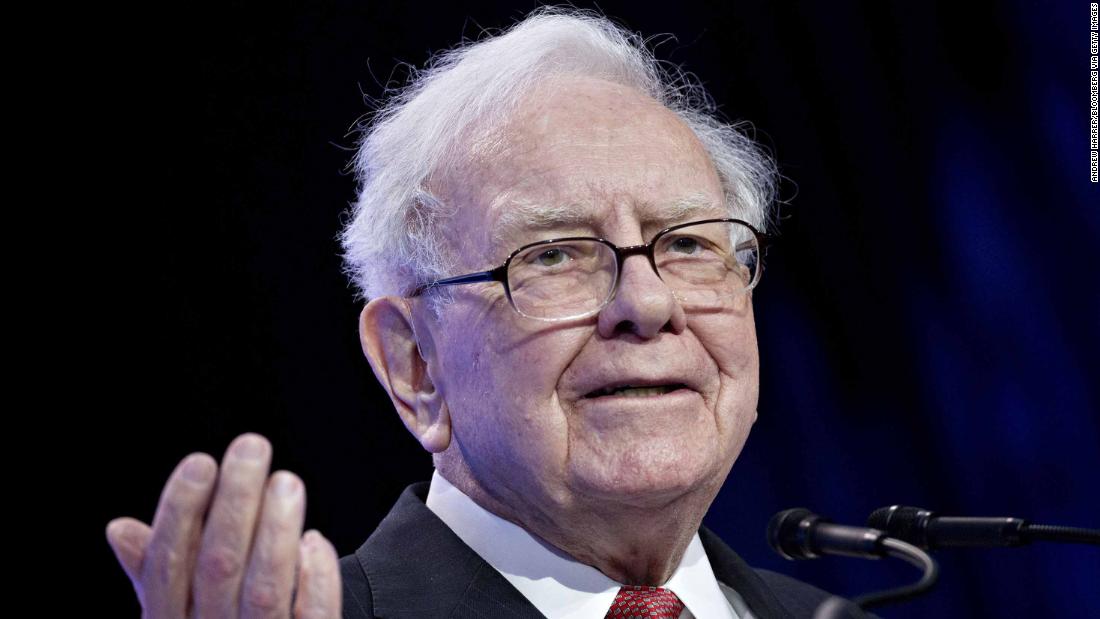

Berkshire on Saturday reported it has $128 billion in cash, up from $122 billion in the second quarter.

Berkshire Hathaway(BRKA) has lagged the market this year, and Buffett has said that he wants to make an "elephant" sized acquisition with the company's mountain of cash. The problem is that the market rally has made any potential targets much more expensive, and Buffett has said he doesn't want to overspend on deals.

Berkshire's operating profit rose to $7.9 billion, up from $6.9 billion a year earlier, boosted by gains across its holdings. The Omaha, Nebraska-based company's performance is tied to its many subsidiaries -- which include GEICO, railroad Burlington Northern Santa Fe and consumer brands like Duracell, Dairy Queen and paint maker Benjamin Moore -- as well as a massive investment portfolio.

While Berkshire has yet to make a major acquisition, the company has been taking steps to embrace more reasonably valued tech stocks in recent years. Berkshire Hathaway still owns large stakes in value stalwarts like Coke,(KO)Bank of America(BAC), Wells Fargo(CBEAX) and Kraft Heinz.(KHC)

But the company's biggest holding now is Apple(AAPL), and Berkshire even has a small stake in Amazon(AMZN).

Berkshire Hathaway also purchased $700 million of its own stock in the third quarter, an uptick from the $442 million it bought last quarter. The company purchased $1.7 billion of its own shares in the first quarter.

Previously, the company did not allow stock buybacks. The board changed a rule last year to allow the company to begin purchasing back billions of dollars worth of stock, a practice that has been criticized by some analysts as inflating share prices.

PARIS—

Carlos Tavares

stunned the auto world when he left his post as heir apparent to

Carlos Ghosn

at the globe-spanning Renault-Nissan alliance six years ago and then took the reins of struggling rival Peugeot, which sold relatively few cars outside Europe.

Now the 61-year-old chief executive of Peugeot’s owner, PSA Group of France, is stepping back onto a wider stage. Mr. Tavares negotiated a nearly $50 billion merger with

Fiat Chrysler Automobiles

FCAU 2.74%

NV that, if completed, will mark one of the biggest auto-industry deals in decades and leave him CEO of the combined company.

The deal presents Mr. Tavares with new challenges. He rescued Peugeot largely by cutting costs and focusing on the bottom line, and he has touted the virtues of staying nimble rather than chasing scale in a rapidly changing industry.

“We are not market-share addicts,” Mr. Tavares said in a March interview with The Wall Street Journal. “We believe agility is very important.”

Yet the proposed merger would create one of the world’s largest car companies, an auto-making behemoth with a major North American presence and nearly a quarter of the European market.

Peugeot was bleeding cash when it recruited Mr. Tavares in 2013. Under his leadership, PSA has gone from losing €5 billion (about $5.6 billion) in 2012 to last year reporting a net profit of €3.3 billion, with a margin of 8.4% in its core automotive business, making it among the most profitable mass-market car makers in the industry.

He achieved the turnaround in large part by slashing production and preaching the dangers of expanding too fast or chasing sales with discounts. He also trimmed the workforce without closing factories, negotiating an agreement with unions to cut the standard workweek for some employees and eliminate jobs through buyouts.

“One of the challenges for us is to keep that near-death experience alive,” Mr. Tavares said in a 2017 interview with the Journal. “It teaches you what you really need to do.”

But he also saw that scale was vital for survival as the global auto industry heads into its next downturn, according to people familiar with his views.

PSA was in danger because of its reliance on Europe’s sluggish market. In 2018, PSA sold 3.95 million vehicles, compared with 10.85 million for

Volkswagen AG

and 10.4 million for

Toyota Motor Corp.

Nearly 80% of PSA’s sales were in Europe.

For months, PSA and Fiat Chrysler have been holding on-again, off-again talks about teaming up, according to people familiar with the discussions. The conversations were briefly interrupted in May by Fiat Chrysler’s failed attempt to merge with Renault, but resumed again over the summer.

In recent weeks, Mr. Tavares approached Fiat Chrysler with a plan to merge the auto makers—a goal that long eluded both Mr. Ghosn and Fiat Chrysler’s former CEO,

Sergio Marchionne,

who died in 2018.

While those auto executives were famous workaholics—jetting around the world to make factory visits—Mr. Tavares is a strict practitioner of work-life balance. His workday generally runs from 8 a.m. to 6:30 p.m., and he makes calls on the drive home before taking the evening off.

He spends many of his weekends at the track, racing cars and competing in events like the 24-hour Le Mans Classic. Last year, he ended that race by spinning off the track in his Lola T70, a classic British race car, before colliding with another car.

“I’m in favor of a life in which you’re not bored to death,” he told motor racing publication Endurance-Info afterward.

Mr. Tavares studied engineering in Paris before joining Renault in 1981 as a test-driving engineer.

He quickly climbed through the ranks. After a stint in the vehicle-development unit of

Renault SA

’s alliance partner,

Nissan Motor Co.

, Mr. Tavares took charge of the Japanese auto maker’s operations in North and South American. There he increased U.S. market share a full percentage point to 8.2% at the height of the recession that followed the 2008 financial crisis. That positioned him to return to France as Mr. Ghosn’s No. 2.

But Mr. Tavares bristled in Mr. Ghosn’s shadow, telling Bloomberg News in 2013 his boss was “here to stay” and musing about running

General Motors

Co.

“Why not GM?” he said. “I would be honored to lead a company like GM.”

SHARE YOUR THOUGHTS

What should Mr. Tavares’s priorities be following the merger? Join the conversation below.

Months after he left Renault, Mr. Tavares took over at Renault’s rival in France: Peugeot. At PSA, Mr. Tavares took a page out of Mr. Ghosn’s playbook by cutting costs and maintaining a sharp focus on key metrics. Mr. Tavares himself was known for flying on budget airlines rather than the private jets used by many auto titans.

PSA quickly returned to profitability, and Mr. Tavares got to work making the company bigger.

In 2017, Mr. Tavares increased PSA’s share of the European market with the acquisition of Opel and Vauxhall from General Motors, which sold after years of losses.

A review of Opel’s costs compared with PSA’s was revealing: At some of Opel’s German manufacturing plants, costs were around double that of PSA’s French plants. That sparked a strong reaction among Opel employees who felt challenged to do better, Mr. Tavares said in an interview at the time.

“First they got scared and then they got excited,” he said.

As well as cutting jobs and pushing further into electric vehicles, Mr. Tavares accelerated plans to shift production to the French car maker’s technology, allowing the larger car group to save money by building Peugeot, Citroën, Opel and Vauxhall models with the same equipment and parts.

Last year, Opel reported a 4.7% operating margin, marking its first profitable year since 1999.

Robert Peugeot, who heads the Peugeot family’s investment firm, said recently, “I was flabbergasted to see how fast the recovery was achieved.”

(Bloomberg) -- Berkshire Hathaway Inc.’s operating profit jumped 14% to a record as Warren Buffett’s conglomerate saw gains from its railroad and got some long-awaited earnings from Kraft Heinz Co.

Operating earnings climbed to $7.86 billion in the third quarter as investment income rose and Berkshire’s reinsurance group had the first underwriting profit in more than a year despite losses from a Japanese typhoon. Revenue climbed 2.4% on increases from the company’s insurers and manufacturing businesses.

The results pushed Buffett’s cash pile to a record $128 billion, even as he completed a $10 billion investment in Occidental Petroleum Corp., his chunkiest purchase in more than year. Aside from that deal, Buffett was a net seller of stocks in the quarter and bought back less of Berkshire’s own shares than some analysts expected, raising more questions over how long the legendary investor will wait to use his dry powder.

The fact that Buffett’s sprawling businesses are spitting out cash faster than he can find good places to invest it is a problem many companies would envy. But there are signs that the idle funds are weighing on growth, and Berkshire’s stock is on track for its worst underperformance since 2009. The company’s Class A shares gained 5.7% this year through Friday’s close, short of the 22% climb in the S&P 500 Index during that time.

Berkshire recognized $467 million in gains related to its share of Kraft Heinz’s profit in the first nine months of 2019. The gains came all at once after the stake left a blank spot in Berkshire’s results for two quarters as the packaged food giant delayed reporting results amid regulatory probes.

Buffett has been stung by Kraft Heinz’s stumbles over the past year. After Kraft Heinz announced a $15.4 billion writedown in February, Berkshire said it would take a $2.7 billion charge on its stake. Kraft Heinz released first-half results in August and was back on track in October, when it reported third-quarter profit that beat analyst estimates. That sent shares climbing to their highest level since May, though they’re still well below Berkshire’s carrying value. Berkshire said Saturday it didn’t believe an impairment charge was necessary at this time.

Buffett’s railroad was able to open up all key routes in the third quarter that had been impacted by flooding. The 5% profit gain at Berkshire’s railroad, BNSF, also benefited from higher rates on shipments even as volumes fell.

Berkshire’s $700 million of repurchases in the quarter was a nearly 75% increase from the amount of stock the company bought back in the second quarter. Still, third-quarter buybacks fell short of Berkshire’s record repurchase of $1.7 billion stock in the first quarter and was lower than the $900 million estimated by analysts at UBS Group AG.

While Buffett received more flexibility to buy back shares last year, his repurchases have been modest compared to other giant companies, especially financial firms. Bank of America Corp. said in June that it planned to repurchase more than $30 billion of its stock over the next year.

More key figures from the results:

Pretax earnings from Berkshire’s group of manufacturers, which includes Precision Castparts Corp. and Marmon, jumped 4.9% in the third quarter. That was boosted by gains at Precision due to demand for aerospace products and increases at Clayton Homes, which manufactures mobile homes and has been expanding into site-built construction.Net earnings slipped 11% to $16.5 billion. Under new accounting rules, Berkshire has to report swings in its investment portfolio in its net income figures. The unrealized gains during the third quarter were about $8 billion compared to a gain of $10.2 billion in the same period a year earlier.

(Updates with details throughout.)

To contact the reporter on this story: Katherine Chiglinsky in New York at kchiglinsky@bloomberg.net

To contact the editor responsible for this story: Michael J. Moore at mmoore55@bloomberg.net

For more articles like this, please visit us at bloomberg.com

The Canadian Press Published Saturday, November 2, 2019 6:43AM EDT Last Updated Saturday, November 2, 2019 6:50AM EDT

OTTAWA -- The Canadian Food Inspection Agency say Sobeys Inc. is recalling Compliments brand fresh cut vegetable products due to possible Listeria contamination.

The products, which include Sweet Kale Blend, Vegetable Platter with a Ranch Dip, Broccolini, Cauliettes -- Chopped Cauliflower, Power Green Blend and Green Beans, all have best before dates of Oct. 31, 2019.

They were sold across Canada, and anyone who has them should either throw them out or return them to the store where they were purchased.

There have been no reports of illness linked to the products, however, Listeria poisoning symptoms can include vomiting, nausea, fever, muscle aches, severe headache and neck stiffness.

This report by The Canadian Press was first published on Nov. 2, 2019.

from Business - Latest - Google News https://ift.tt/2ppWeHa

via IFTTT

November 02, 2019 at 05:43PM

“Lookin’ for love in all the wrong places/

Lookin’ for love in too many faces/

Searchin’ their eyes and lookin’ for traces/

Of what I’m dreamin’ of”

“Looking for Love” — Johnny Lee

Peugeot (PSA) and Fiat Chrysler Automobiles (FCA), it was revealed this week, are looking to tie the knot.

It’s not, shall we say, the first trip to the altar for either brand, Peugeot, for instance, having recently bought GM’s failing Opel and Vauxhall divisions as part of a 2016 expansion mandate. It has also owned Citroen since 1976 and, like so many other companies looking for rapid expansion, created a luxury division – DS – in 2009.

But compared to Fiat Chrysler, Peugeot is the proverbial vestigial virgin. Not only is the current iteration of the multi-national conglomerate a who’s who of the previously unloved – FCA’s current brands include Abarth, Alfa Romeo, Chrysler, Dodge, Fiat, Jeep, Lancia, Maserati and Ram trucks, not to mention Ferrari which it just spun off – in recent years it has become the Elizabeth Taylor of auto companies, having wed, or been affianced to, seemingly every automaker of note.

First there was Daimler, with whom it was legally betrothed. But since that “partnership” ended in acrimonious divorce in 2007, FCA has courted General Motors, BMW, Volkswagen and, most recently, Nissan-Renault, FCA always the pursuing party. Hell, this is the second time FCA has been seen chasing the French automaker, the Financial Times reporting that Auburn Hills (by way of Italy) was trying to woo Peugeot just before its embarrassing dalliance with Nissan-Renault.

Indeed, of the “biggies,” perhaps the only automaker FCA has seemingly never eyed is Toyota. (I suspect that, having learned a lesson with the regimented Germans, even the most optimistic suitor determined the even more buttoned-down Toyota was not marriage material.) To even the casual observer, Fiat Chrysler’s entreaties smack of the kind of cloying desperation seldom seen in the business world.

And for any union to work – especially business unions, even more than personal affairs – there has to be a tangible benefit for both parties. Beyond the always-promised “economies of scale” – and that wasn’t enough to keep DaimlerChrysler together – there doesn’t seem to be much gained other than bragging rights (the union would vault Peugeot-Fiat Chrysler to fourth largest among the world’s automakers).

One of the supposedly important benefits, claim the analysts, is FCA helping Peugeot re-establish itself in the North American market, the French automaker eyeing a return for about five years now. Uhm, note to Carlos Tavares (currently CEO of Peugeot): Don’t you think that, if FCA really had any idea how to market small European hatchbacks to Americans, it would have already done so with Fiat?

Nor do there seem to be many synergies. Peugeot does make some darling little motors, but Fiat’s failure in North America has nothing to do with technology. Neither party has tremendous expertise in the Far East, and both are fairly non-existent in South America. As Bernstein analyst Max Warburton told the Financial Times, “It’s obvious that PSA does not offer any synergies in the U.S., and very little in LatAm. Putting PSA and FCA together in China doesn’t solve much either: two wrongs don’t make a right.” Other than Peugeot getting access to a few Jeep platforms, it’s tough to see what all the hoopla is about.

The one significant benefit that might be tangible is electric vehicles, both companies struggling to comply with various governments’ EV mandates. But, as Mazda has just proven with its new MX-30, being a (relatively) small automaker does not preclude bringing real innovation to the EV segment. Indeed, with so much of battery and EV propulsion technology being developed by outside consultants, electric vehicles alone would not seem reason enough to be eternally wed.

PSA Peugeot Citroen Chief Executive Carlos Tavares delivers a speech during the presentation of the company’s 2018 full year results, in Rueil Malmaison, west of Paris, Tuesday, February 26, 2019.Thibault Camus / Getty

Nor is this likely to be an easy conjoining of personalities. Officially, the management structure is to have Carlos Tavares as the CEO of the merged company, the position he now holds with Peugeot. Similarly, John Elkann will be the union’s board chairman, the title he currently enjoys at Fiat Chrysler.

But how long will all this kumbaya-ness last? Tavares, as you may remember, jumped ship from Renault to Peugeot not two weeks after being rebuffed in his demand to be made top dog there. And anyone who has followed the Agnelli dynasty – Elkann is the grandson of legendary Italian industrialist Gianni Agnelli – knows they are Italian royalty and always expect to be treated as such.

Note to Carlos Tavares: Don’t you think if FCA knew how to market small European hatchbacks to Americans, it would have done so with Fiat?

Why this union of management should go any better than any other – DaimlerChrysler, for instance, was a hot mess right from the get-go and the intrigue that has plagued Nissan-Renault these last 12 months has been truly disturbing – is not exactly clear.

Nor is it proven that bigger is always better. DaimlerChrysler didn’t work. General Motors is much better off since it jettisoned about half its brands. Ford, meanwhile, thinks that rationalization – it’s dumped nearly all of its passenger cars in favour of focusing on trucks and SUVs – rather than expansion of its product line is the key to future success. Indeed, even FCA itself provides no proof that mergers work. Yes, Chrysler avoided a government buyout, but Fiat has been an abject failure in North America and Magic Wagons are not exactly a plague on Italian highways.

Indeed, in the end, one can’t help ask why they either party felt the need to rush into marriage. Why couldn’t they, like so many other modern automakers, just sleep around? Ford and General Motors didn’t walk down the aisle to produce new 10-speed transmissions. BMW, Mercedes-Benz and Audi didn’t propose some form of polyamorous merger when they decided to cooperate in developing autonomous driving technology.

Even the most schoolmarm-ish of automakers, Toyota, has resorted to inter-automaker promiscuity, having created an entire sports car portfolio from trysts with multiple partners. Its Supra, as seen in all the news lately, is the result of a recent affair with BMW, while its lesser sportster, the 86–née-Scion-FR-S, is the out-of-wedlock progeny of a fling with Subaru. And don’t tell me there’s no loyalty without matrimonial blessing; so happy is the world’s largest automaker with its dalliance that it’s commissioned a second-generation GT to keep the blood-, er product-, line going.

So, the question is not so much why these two automakers feel the need to sleep – er, work – together, but why is FCA seemingly so eager to put a ring on Peugeot’s finger?

from Business - Latest - Google News https://ift.tt/2WAY4AO

via IFTTT

November 01, 2019 at 05:53PM

An employee in a branded helmet is pictured at Saudi Aramco oil facility in Abqaiq, Saudi Arabia October 12, 2019.

Maxim Shemetov | Reuters

Saudi Arabia's Crown Prince Mohammed bin Salman on Friday agreed that the initial public offering of state oil giant Aramco will be announced on Sunday, five sources familiar with the matter told Reuters.

The world's top oil company will announce its intention to float on Nov. 3, the sources said.

"The crown prince finally gave the green light," one source said.

Aramco declined to comment.

Saudi Aramco officials and advisers have held last-minute meetings with investors over the past few days in an attempt to achieve as close to a $2 trillion valuation as possible ahead of an expected listing launch on Sunday, according to sources.

The final meeting by the Saudi government on Friday evening was to decide whether to go ahead with the listing.

To achieve $2 trillion, in the largest IPO in history, Riyadh needs the initial listing of a 1%-2% stake on the Saudi stock market to raise at least $20 billion-$40 billion.

The listing is the centerpiece of the crown prince's plan to shake up the Saudi economy and diversify away from oil. But there have been various delays since it was first announced in 2016.

Prince Mohammed wants to eventually list a total of 5% of the company. An international sale is expected to follow the domestic IPO.