Hudson’s Bay Co. (HBC.TO) Executive Chairman Richard Baker is spearheading an attempt to take the retailer private.

Baker is leading a group that owns 57 per cent of HBC’s common shares and is proposing to buy full control of HBC at $9.45 per share, compared to Friday’s closing price of $6.37.

The company's shares ended Monday trading up 42.23 per cent - or $2.69 - at $9.06.

“While we continue to believe in HBC’s long-term potential, it has become clear that the significant challenges, risks and uncertainties facing HBC in the rapidly evolving retail environment are best addressed in a private market setting,” Baker said in a release Monday.

In a separate release, HBC said its board has formed a special committee to consider the privatization proposal, which was delivered more than a decade after Baker’s private equity firm swept in to buy the company as a building block in a growing retail industry empire.

The Baker-led group’s announcement came a few minutes after HBC announced it would raise $1.5 billion by selling its stake in a German real estate joint venture and some related assets. The company also said it will review options for operations in the Netherlands.

Baker’s group said in a release their proposal in conditional on HBC closing the European asset sales that were announced Monday.

Bank of America Merrill Lynch and RBC Capital Markets are serving as financial advisors to the Baker-led group, which also includes Rhône Capital, WeWork Property Advisors, Hanover Investments (Luxembourg) S.A., and Abrams Capital Management.

from Business - Latest - Google News http://bit.ly/31qGxh4

via IFTTT

June 10, 2019 at 08:18PM

NANAIMO, B.C. - Tilray Inc. (TLRY.O) has signed a deal that puts limits on how and when its largest shareholder may sell its stake in the cannabis company.

Privateer Holdings Inc., one of the company's early investors, holds 75 million Tilray shares, roughly a 77 per cent stake in the Canadian company.

Under the agreement, Tilray will acquire Privateer and its stake in the company in exchange for an equal number of new Tilray shares that will be issued to the U.S. private equity firm's shareholders.

The new shares will be subject to a lock-up and may only be sold under certain circumstances over a two-year period.

During the first year, the shares will be released only in marketed offerings and/or block trades to institutional investors or via sales to strategic investors arranged at the sole discretion of Tilray.

The remaining shares will be subject to a staggered release over the second year.

from Business - Latest - Google News http://bit.ly/2KETait

via IFTTT

June 10, 2019 at 08:14PM

OPEC’s oil production dropped by 170,000 bpd from April to 30.09 million bpd in May—the lowest level since February 2015, as Saudi Arabia cut its oil output even deeper despite the end of the U.S. sanction waivers for Iranian oil customers, according to the monthly S&P Global Platts survey.

According to the survey that measures well-head crude oil production in each OPEC state, the cartel’s largest producer Saudi Arabia further slashed its production in May—by 120,000 bpd from April to 9.7 million bpd last month. This was the lowest Saudi oil production in four and a half years, according to Platts estimates.

At the end of May, a Reuters survey showed at that although OPEC’s oil production dropped to a 2015 low of 30.17 million bpd in May, Saudi Arabia boosted its production by 200,000 bpd. This rise in Saudi supply, however, was unable to offset an even larger production decline in Iran after the U.S. removed all sanction waivers at the beginning of May.

Yet, even with the 200,000-bpd boost in May estimated by Reuters, Saudi Arabia was comfortably below its 10.311-million-bpd cap under the OPEC+ deal as it had been overachieving in its share of the cuts by 500,000 bpd in the previous months.

The Platts survey showed that the Saudis appear to have cut deeper last month, despite the end of the U.S. waivers for Iranian buyers and the opportunity to increase the Saudi market share at the expense of Iran.

OPEC will release its official crude oil production data for May in the Monthly Oil Market Report (MOMR) on Thursday, June 13, weeks before OPEC and allies are set to discuss the fate of their production cut pact currently expiring at the end of June.

The Canadian Press Published Monday, June 10, 2019 11:51AM EDT Last Updated Monday, June 10, 2019 12:47PM EDT

OTTAWA -- Having the money in the Canada Pension Plan fund actively managed by investment experts has been worth nearly $50 billion in extra returns since the mid-2000s, says the parliamentary budget officer.

In a report Monday, the PBO compared the growth in the $392-billion public pension fund to what the same money would have made in "passive" investments that just tracked a pair of index funds, and finds the active-management strategy has come out ahead.

Passive investments have almost no expenses because there's very little buying, selling or research involved in managing them. Some personal-finance experts say passive investments are good for most people's retirement savings because professional money managers don't add enough extra value to make up for what they cost in higher fees.

The Canada Pension Plan Investment Board switched to active management in 2006.

"Given that active management requires more personnel to conduct the required research, and also involves more transactions, this strategy comes with increased complexity and additional costs," the PBO report says. "The goal is that in the long run, after netting these costs, the strategy will achieve a higher return than an identified benchmark."

So far, so good, the analysis found: In each of the 12 full years the investment board has been using the active-management approach, including in the recession at the end of the 2000s, it's brought better returns than passive investing.

Even when all the extra costs of active management of the Canada Pension Plan fund are accounted for, its experts' wheelings and dealings are worth an extra 1.2 per cent in investment returns in an average year. That's added up to $48.4 billion in extra investment profits.

A similar analysis of the pension fund for federal workers found that its managers weren't as successful, but still performed slightly better than passive investments would have over the last decade or so.

The PBO found their work has been worth an extra 0.3 per cent in returns each year, after the costs of active management were taken into account, which means $1.7 billion more in the $153-billion fund.

from Business - Latest - Google News http://bit.ly/2I5ICqN

via IFTTT

June 10, 2019 at 10:51PM

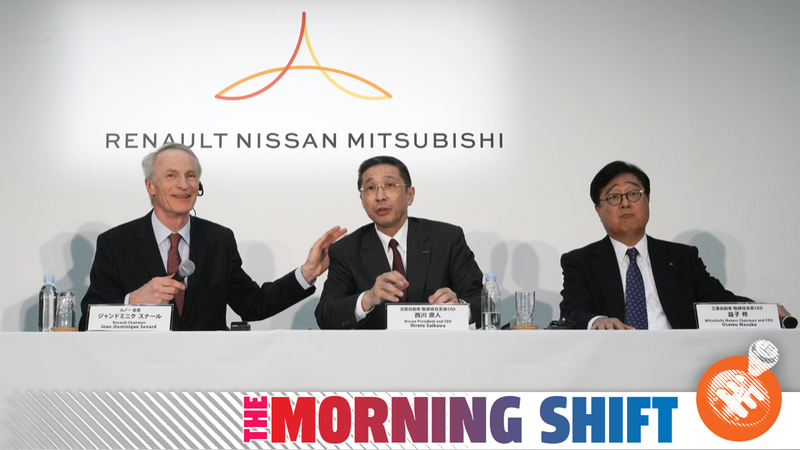

Strains within the alliance between Renault and Nissan increased today as the Japanese car maker criticised its French partner for failing to back its governance reforms.

The tensions that have been simmering beneath the surface since the arrest in November of Carlos Ghosn, the alliance’s former head, burst into the open after Renault complained that it was being sidelined by Nissan.

In an unusally public display of anger, Hiroto Saikawa, 65, Nissan’s chief executive, denounced Renault’s stance as “most regrettable”.

The alliance between Nissan, Renault and Mitsubishi — once the most successful of its kind in the world — is in crisis after Mr Ghosn, 65, was charged with under-reporting his salary and misuse of corporate funds.

Nissan, which caused Mr Ghosn’s downfall when it…

from Business - Latest - Google News http://bit.ly/31qGphA

via IFTTT

June 10, 2019 at 11:00PM

President Donald Trump on Monday said he has concerns that a merger between United Technologies and Raytheon would harm competition and make it more difficult for the U.S. government to negotiate defense contracts.

"I'm a little concerned about United Technologies and Raytheon," Trump said in an exclusive interview with CNBC. Aerospace companies have "all merged in so it's hard to negotiate" with them, he added, suggesting the defense industry could be heading in the same direction.

Asked whether he would have problems with the merger, Trump replied, "Only if they have the same products. That would be the thing that bothers me most."

United Technologies and Raytheon announced on Sunday that they had struck deal to combine, which would bring together a booming aerospace business with a giant government defense contractor. That tie-up could rattle suppliers, customers and competitors. The new company, with an estimated $74 billion in sales, would become the second-largest aerospace-and-defense company in the U.S. after Boeing.

Executives from the two companies dismissed Trump's concerns about a possible reduction in competition, saying they have very little overlap that would generally spark concern among anti-trust regulators.

"We are complementary, not competitive," Raytheon CEO Tom Kennedy told CNBC in an interview. "I don't know the last time we competed against United Technologies."

Greg Hayes, United Technologies' CEO and chairman who is slated to be CEO of the new company, once the merger closes, said he looked forward "to talking to the president later today," about potential job growth under the deal.

Still, the president repeatedly expressed concerns about dwindling competition in aerospace.

"When I hear United and I hear Raytheon, when I hear they're merging, does that make it less competitive? It's already not competitive," Trump said.

"I just want to see competition. They're two great companies, I love them both. But I want to see that we don't hurt our competition."

The proposed deal would create a giant, one-stop shop with products that range from Tomahawk missiles and radar systems to jet engines that power passenger planes and the seats that fill them.

Raytheon and United Technologies have a combined market value of close to $166 billion. The stock price of each has gained more than 21% this year, far outpacing the broader market, as they've reaped the benefits of strong defense spending and record orders for passenger planes around the world. Still, they have lagged some of their competitors.

United Technologies is in the process of spinning out its Carrier air conditioning unit and its Otis elevator business. The company expects those transactions and the newly announced deal with Raytheon to close by early 2020.

Everything is falling apart for Renault-Nissan, more tariff threats, more Brexit fallout, more alleged corruption in the Trump administration, and bad reviews for Elon Musk as a boss. All this and more in The Morning Shift for Friday, June 10, 2019.

1st Gear: Renault-Nissan Tensions Get Even Tenser

As you may be aware, Nissan’s former chairman and CEO Carlos Ghosn is currently awaiting trial in Tokyo for a slew of corruption-related charges. One of the major issues brought to light by Ghosn’s arrest has been how Nissan’s corporate structure enabled his alleged malfeasance. At the very least, it’s clear there are, ahem, problems with Nissan’s corporate structure that allowed one person to wield so much power.

Which brings us to this weekend, when Renault, which had previously been supportive of Nissan’s internal reform efforts, notified the Japanese automaker that they will not, in fact, be voting for the governance reforms on the table, both Bloomberg and Reuters reported. This is a very big problem for Nissan, because such a move requires two-thirds of shareholders to vote in favor, and Renault owns 43 percent of Nissan. Without Renault’s support, the measure cannot pass.

What is Renault’s problem? They don’t think they have enough influence in the new governance structure, of course. From Reuters:

A Renault source said Senard’s letter was motivated by concern about Renault’s under-representation on the new Nissan board committees being introduced following the arrest of Ghosn, who is now awaiting trial and denies the financial misconduct charges against him.

“It’s not a final abstention, and Renault’s position can still change,” the source said. “As things stand, Renault has not been assured of appropriate committee representation as Nissan’s main shareholder.”

Renault had yet to receive specific details on the proposed composition of each of the committees, another source with knowledge of the issue told Reuters.

Advertisement

This is a lot of boring corporate governance stuff that will, if I had to guess, get sorted in the coming days and weeks. But the bigger picture here is Nissan was at the very least neutral and at the very worst did not support Renault’s proposed merger with FCA. Both Renault and FCA officially blamed the French government, which owns 15 percent of Renault, for the merger falling apart, but Nissan didn’t exactly help.

Bloomberg summarized the rift as such:

Nissan has long complained that the partnership with Renault is unbalanced, and that the French government’s outsize role at Renault, with board representation and extra voting rights, gives the state undue influence over the Japanese carmaker. Nissan owns a 15% stake in Renault, but with no voting rights, and has been seeking more power in the partnership rather than the “closer ties” sought openly by the French state and pursued first by Ghosn and later by Senard.

Advertisement

In short, even though their fates are all largely intertwined, nobody in this alliance thinks they have enough influence over anyone else.

2nd Gear: Trump Threatens Mexico With Tariffs Shortly After Cancelling Tariffs

President Donald Trump said on Monday the United States had signed another portion of an immigration and security deal with Mexico that would need to be ratified by Mexican lawmakers.

He did not provide details but threatened tariffs if Mexico’s Congress did not approve the plan.

As we wrote regarding fuel efficiency standards, big businesses care not so much about what regulations are, but that they are consistent. Especially in the context of multinational automakers with manufacturing plans extending years into the future, predictability is paramount. Whatever you think of Trump’s tariff threats and massive swings in federal regulatory standards, it is not predictable, and that’s bad for automakers.

3rd Gear: UK Car Production Is Tanking Thanks to Brexit

Earlier in the year, several automakers, including Mini, Rolls Royce, Vauxhall, and Land Rover, announced plans to temporarily shut down plants in Britain in anticipation of trade disruptions due to the country leaving the E.U. by March. That “British Exit,” if you will, got pushed back to October, but the plant closures were already in motion. Which resulted in this:

Car production in April fell 24% on the month, the biggest drop since records began in 1995, and the broader category of “transport equipment” showed its largest drop since 1974.

Advertisement

Is that bad?

4th Gear: DOT Secretary Awarding Projects to Help Husband’s Re-Election

The U.S. Department of Transportation head, Elaine Chao, is married to Senate majority leader Mitch McConnell. As it happens, Chao has created a “special path” for DOT projects in McConnell’s state of Kentucky to get funding, according to a POLITICO investigation:

The Transportation Department under Secretary Elaine Chao designated a special liaison to help with grant applications and other priorities from her husband Mitch McConnell’s state of Kentucky, paving the way for grants totaling at least $78 million for favored projects as McConnell prepared to campaign for reelection.

Chao’s aide Todd Inman, who stated in an email to McConnell’s Senate office that Chao had personally asked him to serve as an intermediary, helped advise the senator and local Kentucky officials on grants with special significance for McConnell — including a highway-improvement project in a McConnell political stronghold that had been twice rejected for previous grant applications.

Advertisement

This comes a week after the New York Times investigation detailed how Chao has used her cabinet position to elevate the standing of her family’s shipping company, which has donated millions of dollars to her husband’s campaign.

Surely there is someone else more qualified to run the country’s Department of Transportation who isn’t married to the Senate majority leader or the heiress to a massive shipping company, which is of course regulated by said Department of Transportation. Perhaps the better question: is there anyone less qualified?

5th Gear: Job Ratings Websites Are Souring on Tesla Too

Would I rely on a website like Glassdoor when considering a new employer? Probably not; its ratings are entirely anonymous and the site takes no measures to ensure the reviewer actually worked for—or indeed has any familiarity with—that company.

Advertisement

That being said, this Reuters article is still funny, because they found a new angle rather than the usual bearish market analysts or automotive safety experts to pile on Tesla:

At jobs site Glassdoor, Tesla’s overall company rating fell to 3.2 out of 5.0 stars based on reviews written in the first quarter from a high of 3.6 in 2017, according to historical data compiled by Glassdoor at Reuters’ request. The average rating of the nearly 1 million employers reviewed on the site is 3.4.

Like I said, I wouldn’t take any of this too seriously, at least out of the context of what we already know about working for Tesla, which is that it’s a highly volatile but potentially fulfilling work environment with a healthy dose of hero worship and cult-like atmosphere baked in.

Advertisement

Although, about that hero worship:

In the first quarter, Elon Musk’s CEO approval rating dropped to 52% from 90% in 2017.

Advertisement

Yikes.

Reverse: Trail of Doughnuts

Advertisement

Neutral: What’s the Renault-Nissan Endgame?

Does the latest news alter how you see this quarrel unfolding?