The trade war has increasingly become focused on currencies, with the recent spat with China over the yuan in the spotlight.

The Chinese currency's fluctuation spelled disaster for global equities. Then, when China fixed the yuan higher than where experts expected, markets rebounded.

The volatility will likely continue if currency remains in the forefront of the global dispute, but could do long term damage on the global economy.

Now, amid an ongoing spat with China, the currency war is again front-and-center as the global trade dispute rages. It ultimately amounts to a race to the bottom as countries try to push the value of their currencies lower than competitors in order to gain an advantage in trade. This is also why Trump has said he wants a weaker US dollar.

This runs counter to how countries are supposed to work together in order to achieve a balanced economy. When cooperation breaks down, global markets feel the negative effects. That's exactly what's played out around the world over a series of months — and experts are getting increasingly worried that there's no end in sight.

"The market is going to be very volatile," Dan Ikenson, director of the Herbert A. Stiefel Center for Trade Policy Studies at the Cato Institute told Markets Insider. "A trade war that was supposed to be easy to win seems like it's going to be hanging around for a long time."

The immediate damage a currency war can inflict has been clear in recent days. US equities slid to their worst performance of 2019 Monday — erasing billions of dollars in wealth— when China let the yuan fall below a key psychological threshold. The plunge also marked the currency's lowest level since 2008.

Meanwhile, the Cboe Volatility Index — or VIX, commonly known as the stock market's fear gauge — jumped 32% in a single day. The weakness also extended into major European and Asian indexes. Sharp fluctuations also struck the bond market as 10-year Treasury yields plummeted, pushing the yield curve — a closely watched recession indicator — to its most inverted level since 2007.

Then, on Tuesday, markets stabilized when the People's Bank of China set the daily yuan rate higher than expected and said it did not manipulate the currency after a formal accusation from the US Treasury Department.

The two-day takeaway is clear: currency shenanigans are going to negatively impact market sentiment. And considering the matter is largely unresolved, it's likely that there will be much more volatility in the currency market that finds its way into other asset classes. Many — including Trump— now think the ordeal could last until 2020.

"The markets now are going to be hanging on everything that's stated on trade negotiations," so there will be fluctuations depending on signs of progress, Dom Catrambone, CEO of Whitford Asset Management told Markets Insider. "Now I think people need to be watching their portfolios."

Further, China isn't the only global power Trump has fought. The President also accused his European counterparts of manipulating their currency when the European Central Bank suggested in June it may lower interest rates and purchase another round of assets to offset a slowing economy.

Trump did cool European tensions slightly when he made a deal to increase US beef exports to the EU — a move also designed to support American farmers that are hurt by the China tariffs. But even when announcing the agreement, he spooked European officials when he made a joke about levying tariffs on cars from Europe.

While currency devaluation seems to be the latest bargaining chip in the global trade dispute, the long term impacts of weaker currencies in the US and abroad could be "really bad," Catrambone said.

After all, a strong currency tends to be good for both consumers and consumption. And Ikenson thinks prolonged weakness in the greenback could usher in the next big economic collapse.

"A weaker currency could be inflationary and recessionary" over time, he said.

U.S. stocks tumbled sharply at the open Wednesday, relinquishing the previous session’s healthy rebound and them some, as a number of global central banks adopted easy-money policies in the face of an intensifying trade conflict between Beijing and Washington.

How did benchmarks perform?

The Dow Jones Industrial Average

DJIA, -2.07%

fell nearly 568 points, or 2.2%, to 25,459, the S&P 500 index

SPX, -1.74%

lost 54 points, or 1.9%, at 2,826. Meanwhile, the Nasdaq Composite Index

COMP, -1.54%

shed 1.6% to 7,705, a drop of 128 points.

On Tuesday, the Dow rose 311.78 points, or 1.2%, to end at 26,029.52, while the S&P 500 index climbed 37.03 points, or 1.3%, to close at 2.881.77, while the Nasdaq Composite Index

COMP, -1.54%

surged 107.23 points, or 1.4%, to finish at 7,833.27.

What’s driving the market?

Equity markets looked set to fall at the start of trade on Wednesday, with stocks giving up gains as U.S. Treasury and European government bonds plumbed fresh lows. The 10-year Treasury

TMUBMUSD10Y, -5.42%

fell below 1.70%, falling to an intraday nadir at 1.60%, around the lowest since late 2016, while comparable German bonds

TMBMKDE-10Y, -12.61%

hit a record low at negative 0.59%.

“A sharp decline in yields as the 10-year note falls under 1.65%. This is raising the ‘Fear Factor’ over the impact of the trade war on the economy,” Peter Cardillo, chief market economist at Spartan Capital Securities told MarketWatch.

Adding to market jitters is growing fears of a recession in the U.S. against a weaken economic backdrop throughout the globe.

Central bank’s in India and New Zealand (as well as the Thailand) lowered their domestic interest rates to levels that are lower than had been expected, highlighting anxieties centered on the health of the world-wide economy.

India’s central bank cut its key interest rate for the fourth consecutive time, reducing the repo rate by 0.35% to 5.40% to shore up the economy, while New Zealand’s central bank cut its benchmark interest rate to an all-time low of 1% on Wednesday.

For a second day in a row, the People’s Bank of China set the official midpoint reference for yuan at 6.9996 in Asian hours, but the level approaches the key level of 7, widely viewed as a line in the sand for the currency. The PBOC fixes the currency daily and allows it to move up to 2 percentage points on either side of its midpoint.

A breach of that level on Monday, interpreted by some as an intentional weakening of its currency, helped to ignite a global stock market selloff and slump in bond yields, but markets have so far stabilized, despite the prospect of an uncertain timeline for a Sino-American trade resolution.

Losses for the stock-index futures before the opening bell Wednesday accelerated after President Donald Trump tweeted that the U.S’s “problem is not China - We are stronger than ever, money is pouring into the U.S. while China is losing companies by the thousands to other countries, and their currency is under siege - Our problem is a Federal Reserve that is too..... proud to admit their mistake of acting too fast and tightening too much (and that I was right!).

The president said, the central bank “must cut rates bigger and faster, and stop their ridiculous quantitative tightening NOW,” he tweeted:

“Three more Central Banks cut rates.” Our problem is not China - We are stronger than ever, money is pouring into the U.S. while China is losing companies by the thousands to other countries, and their currency is under siege - Our problem is a Federal Reserve that is too.....

....proud to admit their mistake of acting too fast and tightening too much (and that I was right!). They must Cut Rates bigger and faster, and stop their ridiculous quantitative tightening NOW. Yield curve is at too wide a margin, and no inflation! Incompetence is a.....

The Walt Disney Co.

DIS, -6.17%on Tuesday said beginning Nov. 12, when the entertainment giant’s ambitious streaming service makes its debut, U.S. consumers will be able to subscribe to a streaming bundle of Disney+, ESPN+ and advertising-supported Hulu for $12.99 a month. Disney shares were down 6.5% l after missing estimates for earnings.

Lumber Liquidators Holdings Inc.

LL, -16.02%

reduced its full-year comparable stores outlook to “approximately flat.” Lumber Liquidators shares were falling 14% at the open.

Oil futures sank. U.S. oil prices

CLU19, -3.64%

fell 2.9% at $52.08 a barrel, after gaining 1.9% on the New York Mercantile Exchange on Tuesday.

In Asia, Japan’s Nikkei 225 Index

NIK, -0.33%

fell 0.3%, Hong Kong’s Hang Seng Index

HSI, +0.08%HSI, +0.08%

ended virtually unchanged, adding less than 0.1%, while the CS1 300 index

000300, -0.41%

dropped 0.4%.

The pan-European Stoxx 600

SXXP, -0.14%,

meanwhile, headed 0.4% lower Wednesday, giving up a sharpy early gain.

Stock futures reversed into losses Wednesday, as Walt Disney (DIS) weighed heavily on the Dow Jones today following its fiscal Q3 report. But gold mining ...

View full coverage on Google News

https://www.investors.com/market-trend/stock-market-today/stock-futures-fall-as-walt-disney-weighs-on-dow-jones-today-gold-mining-stocks-rally/

Last week, President Trump threatened to place a 10 percent tariff on $300 billion worth of Chinese imports on September 1 unless trade talks with China showed more sign of progress. Already, America has tariffed $250 billion of Chinese imports at 25 percent, and if tariffs are placed on the $300 billion basket of goods, this would increase tariffs on all Chinese imports to the United States.

President Trump is unhappy that talks last week in Beijing between Chinese officials and U.S. Trade Representative Robert Lighthizer and U.S. Treasury Secretary Steven Mnuchin broke down. He’s also unhappy that China hasn’t followed through on a promise to purchase more U.S. agriculture goods, like soybeans, in exchange for the United States allowing our chipmakers (think Intel and Qualcomm) to supply chips to Huawei, a Chinese telecommunications giant.

There are risks to the president’s strategy. While the trade war has yet to significantly affect U.S. consumers, global business sentiment has been negatively affected as global supply chains have been upended, and the $300 billion basket of goods to potentially be tariffed next month is much more consumer-oriented than the $250 billion basket already tariffed.

China can also attempt to retaliate, even though its ability to do so is limited because it doesn’t buy that many American goods. And even China’s tariffs on U.S. agriculture are more complicated than the media would have you believe. For example, China restricted U.S. pork imports since 2011 by spuriously claiming U.S. pork is unsafe. And because African swine fever (ASF) is wiping out China’s pig population, and pigs eat soybean meal, China is demanding less soybeans generally, even from Brazil.

What’s Behind the Latest News

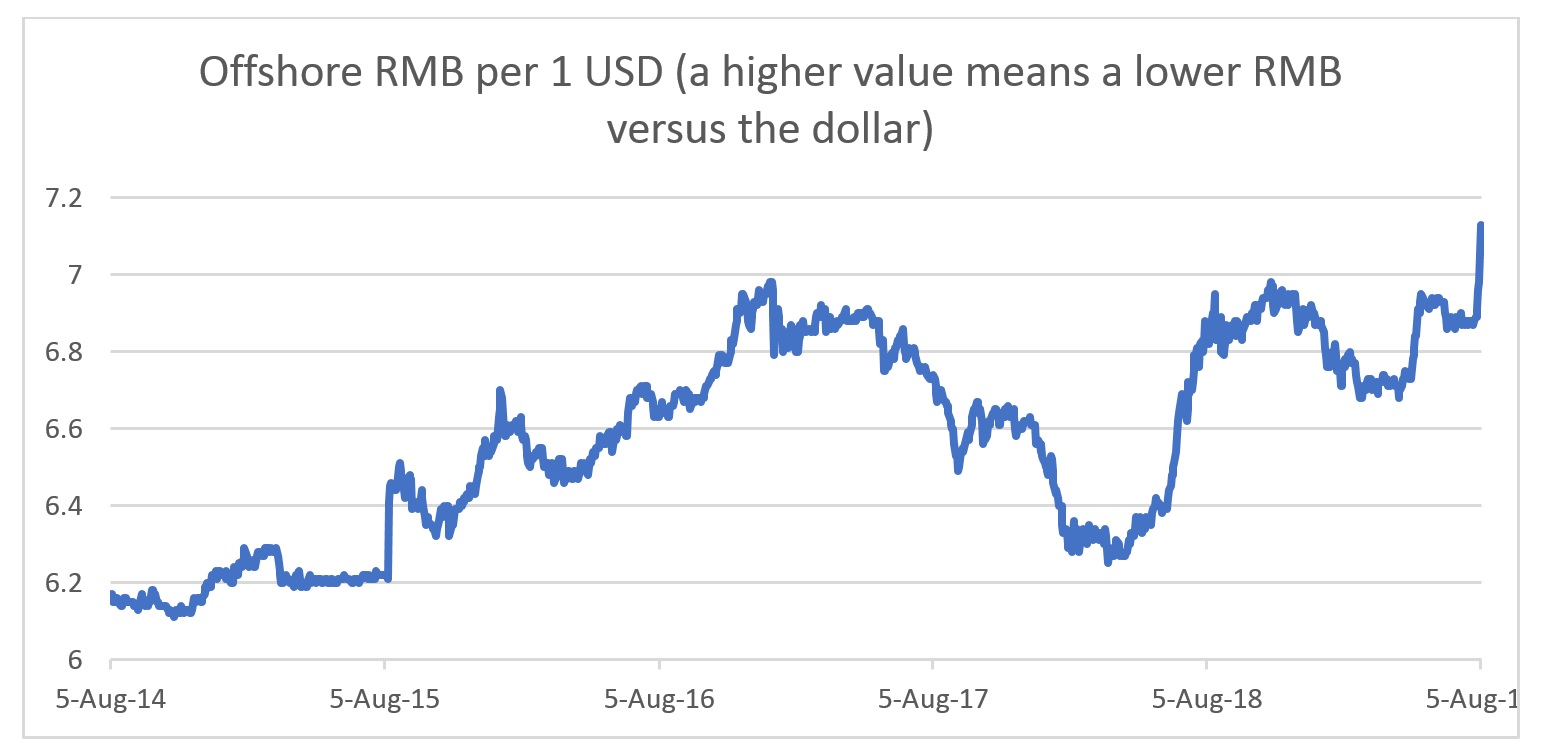

China is responding to Trump’s tariff threat by allowing their currency to weaken versus the dollar.

But the one channel where China could “retaliate” was in their currency rate, because a weaker Chinese currency helps keep Chinese goods attractive to American buyers, despite higher tariffs. China’s currency, called either the yuan or the renminbi (RMB), is pegged by the Chinese central bank (the People’s Bank of China, or the PBOC) to a basket of currencies, chiefly the dollar. The PBOC usually moves the peg higher or lower as it pleases, but market forces also push and pull on it. It is harder for the PBOC to fight the market on a prolonged basis, especially when the RMB wants to move lower.

In years past, China used its peg to suppress its currency value even as it ran huge trade surpluses. In a free market, China’s currency value would rise over time due to the world buying its goods, yet China instead printed RMB and sat on the dollars it received. The RMB printing caused bubbles in China, and sitting on the dollars kept China’s exports super-competitive, by keeping China’s wages artificially low in U.S. dollar terms.

Then several years ago, fearing serial bubbles and a slowing Chinese economy, capital began to flow out of China and the PBOC found itself instead defending its currency from weakening too much. The same is true today—China’s economy is slowing, and coupled with trade tensions with America there is market pressure on the RMB to move lower versus the dollar (in most countries, a slower economy means a lower currency value).

That brings us to Sunday night, when the PBOC allowed the offshore (non-China) traders betting against the RMB to have their way, and the value of the RMB compared to the dollar dropped to the lowest level in years, breaching what traders call the “seven handle” (the dollar now buys more than 7 RMB, up from buying only 6 RMB several years ago).

China’s Move Could Backfire

The PBOC’s move to allow the RMB to weaken against the dollar offsets the sting of tariffs on Chinese exporters, but it carries two important risks for China.

First, that the United States retaliates to the currency devaluation, which is exactly what happened on Monday evening, when the U.S. Treasury Department acted to officially label China a currency manipulator, the first time since the 1990s. The action doesn’t have any immediate consequences, but it acts as a warning to China and can open the door to future penalties on Chinese imports to America.

The second risk is that the PBOC is unable to stop a further RMB slide, which would cause capital outflows and tight money in China, which would crash China’s all-important property market, and thus its economy. It is highly complicated, but even when the PBOC wants easier monetary policy, the stimulus channel is “clogged” if the dollar is rising versus the RMB and money is flowing out of China.

These risks, and the simple fact that the trade war is escalating, explain the market reaction. Equities the world over fell after the announcement. In the United States, the S&P 500 (a good measure of U.S. stock performance) and the Dow Jones Index (a lesser measure of U.S. stock performance) fell by roughly 3 percent, and the NASDAQ index (which is tech stock-heavy) fell by about 3.5 percent.

Here’s the Bigger Backstory

Why Trade Talks Broke Down

President Trump is right: The economic relationship between America and China really is unfair. When Trump took office, the average U.S. tariff on Chinese goods was around 3 percent, and the average Chinese tariff was around 10 percent. A multitude of hidden rules restricted American firms’ ability to do business in China.

Worse, China has long had a quasi-official policy of stealing U.S. intellectual property. U.S. firms that seek to operate in China are forced to partner with a Chinese competitor via “joint venture requirements.” That competitor gets to see their business practices and trade secrets. And to gain a license to operate in China, American firms are forced to hand intellectual property to Chinese officials. Often, these officials give these corporate secrets to local Chinese companies.

China does this because it is obsessed with creating a domestic industry in everything, and is willing to subsidize loss-making companies until they have a foothold. This has worked in some areas—like Huawei with telecoms and China’s train industry—where a firm that was started with stolen technology is now out-competing western firms on their home turf. In other areas—like chipmaking or automobile production—China’s progress has been shoddy, despite access to competitors’ technology.

Some say American companies choose to hand over technology to operate in China. But America doesn’t make Chinese companies do this, and even American companies that don’t operate in China are at risk of Chinese corporate espionage. There are currently almost 1,000 separate FBI investigations into Chinese corporate espionage, at least one in all 50 U.S. states. President Obama got Chinese President Xi Jinping to sign something saying the hacking and theft would stop, but it actually increased the next year.

Trump aimed to fix this, and several months ago his trade team, led by Lighthizer, got China to agree to allow U.S. firms more access to China, increase intellectual property protection and enforcement, and end protectionist measures aimed at restricting the import of U.S. goods, among other things.

But China wanted the United States to remove tariffs immediately, and for political, business, and legal reasons, America wanted to see compliance first. Given history, the Trump administration doesn’t trust that China will stick to its word. The lack of trust wasn’t helped by China, twice at the last minute, trying to change the Chinese-language-version of the trade agreement without America knowing.

China May Never Agree to a Deal

It is highly possible that China never intended to adhere to the terms of a deal. There is a debate as to whether China can politically implement America’s terms or not. But it’s safe to say that enforcing the deal would require Chinese President Xi Jinping to expend a lot of political capital, and even alienate certain politically powerful groups—including Chinese industries that would face competition if American firms and goods were allowed more access to China.

Either way, the talks broke down, and have been stalled for several months. And Trump has so far followed through on his tariff threats.

This Isn’t All about Trade

But this isn’t only about trade. Sometimes stocks are looking for a reason to move lower. The backdrop to all this, which further explains the move, is twofold.

First, people were incredibly on one side of the trade (“net long”) on U.S. equities going into the Federal Reserve rate cut last week, which underwhelmed after U.S. Federal Reserve Chair Jerome Powell tempered expectations for a large amount of future cuts. When traders are crowded on one side of a position, moves can be sharp in the other direction as the popular trade is unwound.

While some on Wall Street have been saying that rate cuts are always bullish for stocks, many are learning otherwise. If the Fed is cutting while the economy is deteriorating—like in the early 2000s or before the Great Recession—stocks can still go down.

The second reason this isn’t all about trade has to do with the global economy. Generally, global economic data has been pretty awful in the last 12 months. Even in the United States, which has been outperforming the rest of the world since Trump’s deregulation and tax cuts, growth is starting to slow.

The big picture behind this slowdown is that the global economy was rolling over in 2015-16, and then the Chinese enacted the biggest stimulus in human history. Global data surged higher, in what Wall Street called the “synchronized global recovery.”

But since last year, Chinese stimulus has run its course, and they can’t stimulate like that again even if they wanted to. That has led to weakness in everything from gauges of Chinese economic activity to gauges of German activity since the back half of last year.

The truth is that the Chinese stock market peaked in late 2017-early 2018. It surged on hopes of a trade war resolution and new Chinese stimulus at the beginning of this year, but those hopes quickly rolled over.

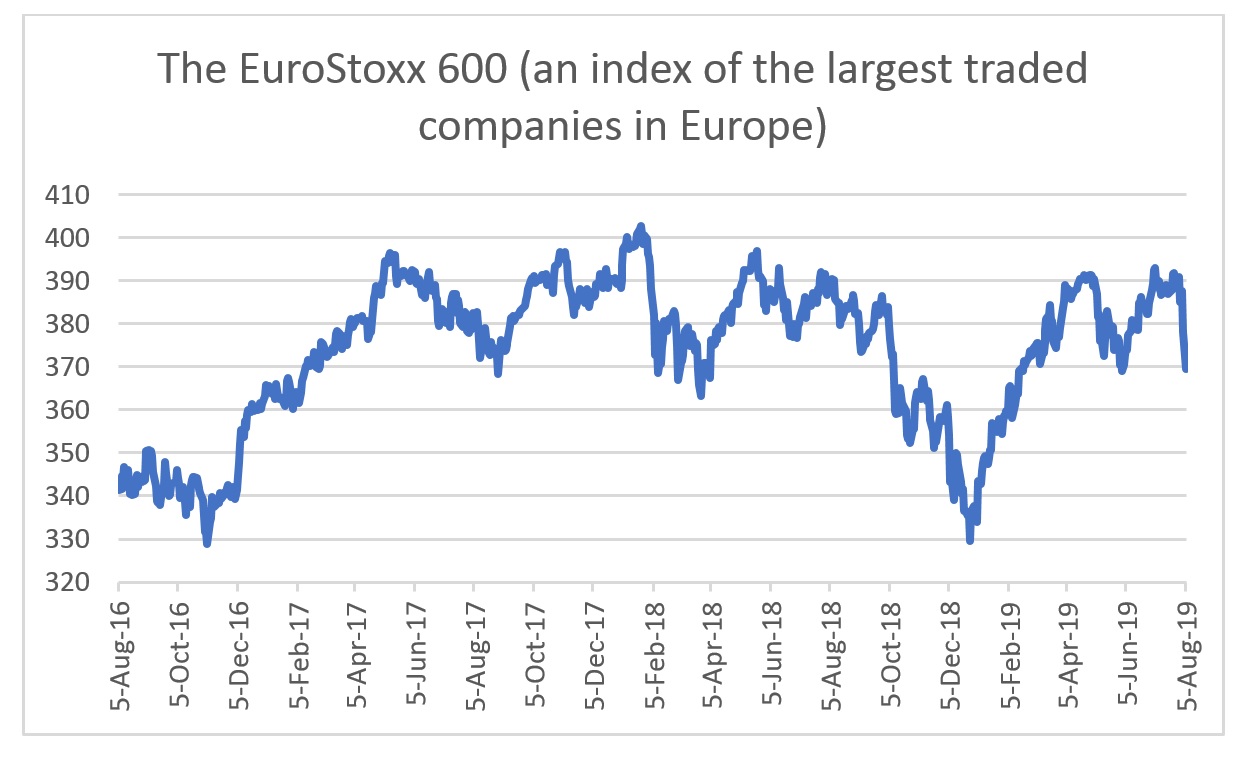

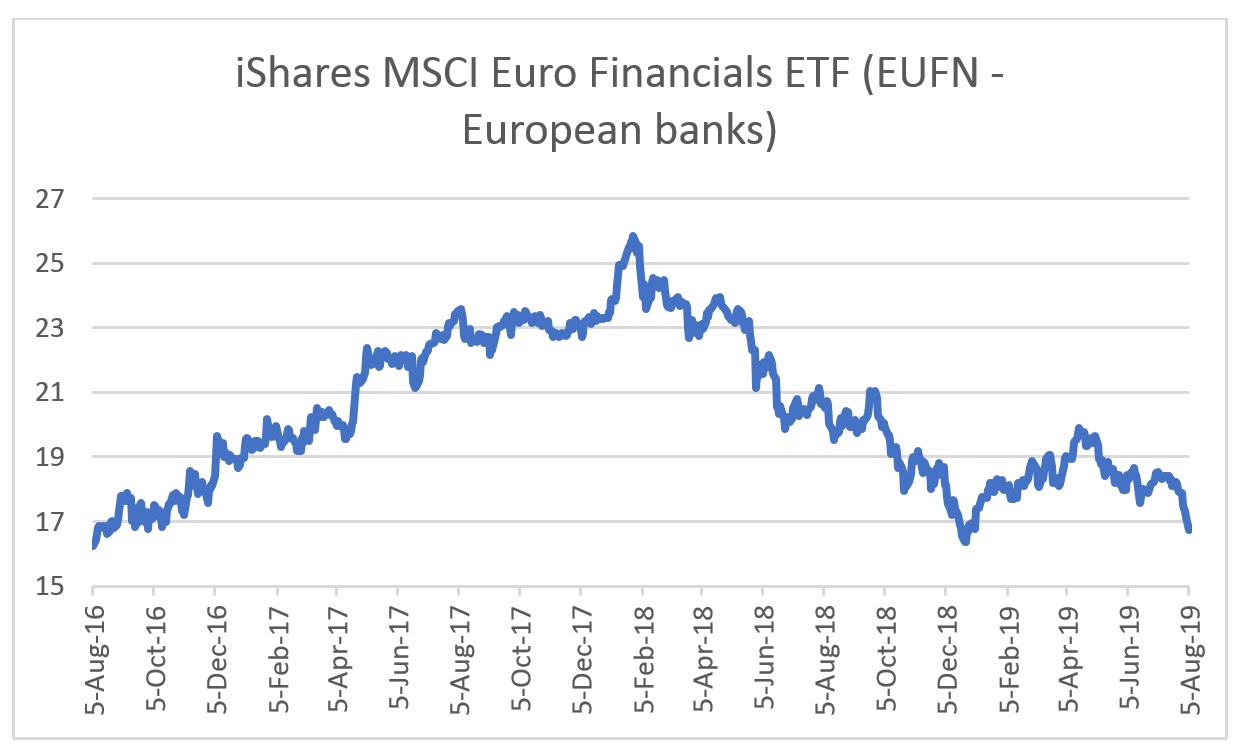

China isn’t an outlier. European stocks also peaked in late 2017-early 2018. Nowhere is this more apparent than Europe’s beleaguered (some would say awful) bank stocks. Again, this has nothing to do with tariffs, and everything to do with the global economic cycle after the massive Chinese stimulus ran its course.

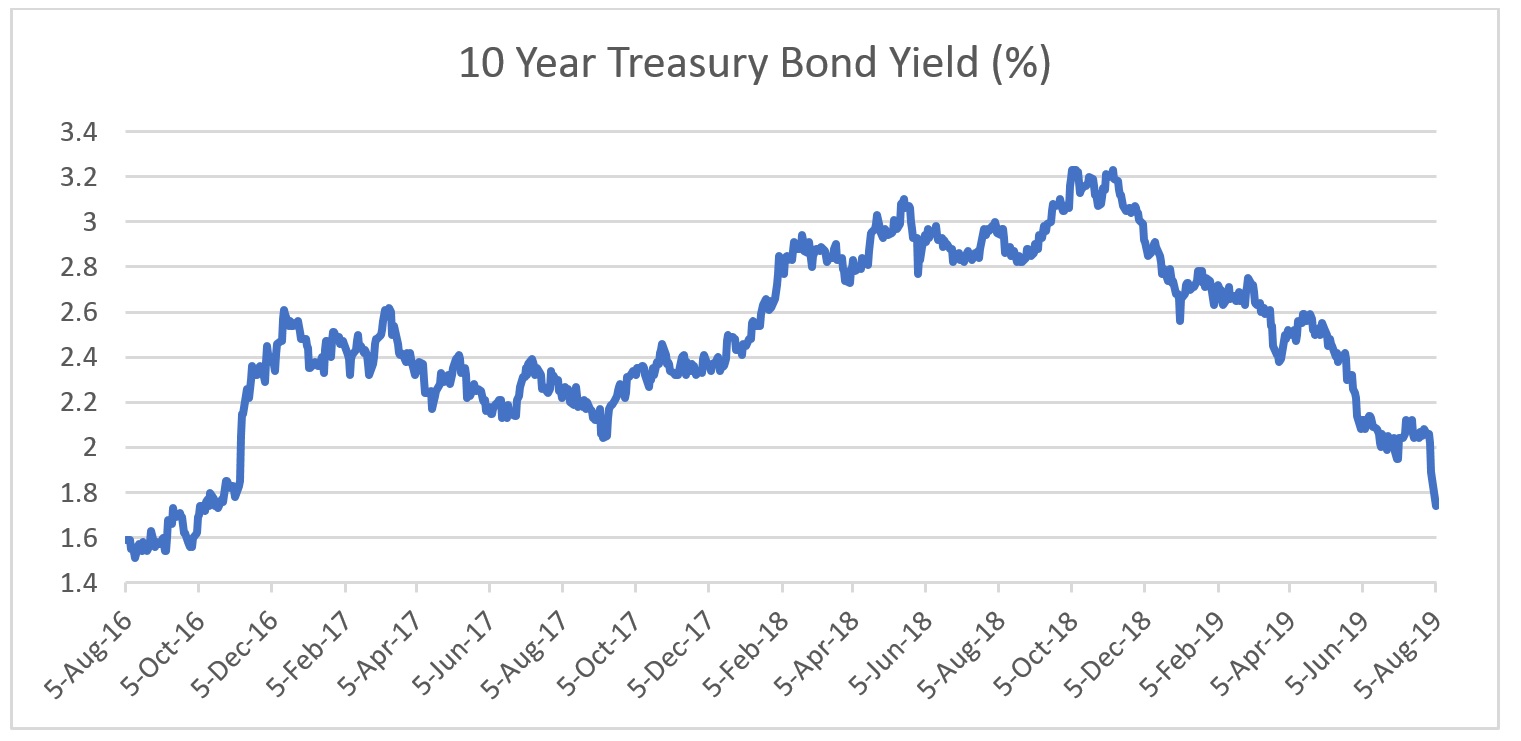

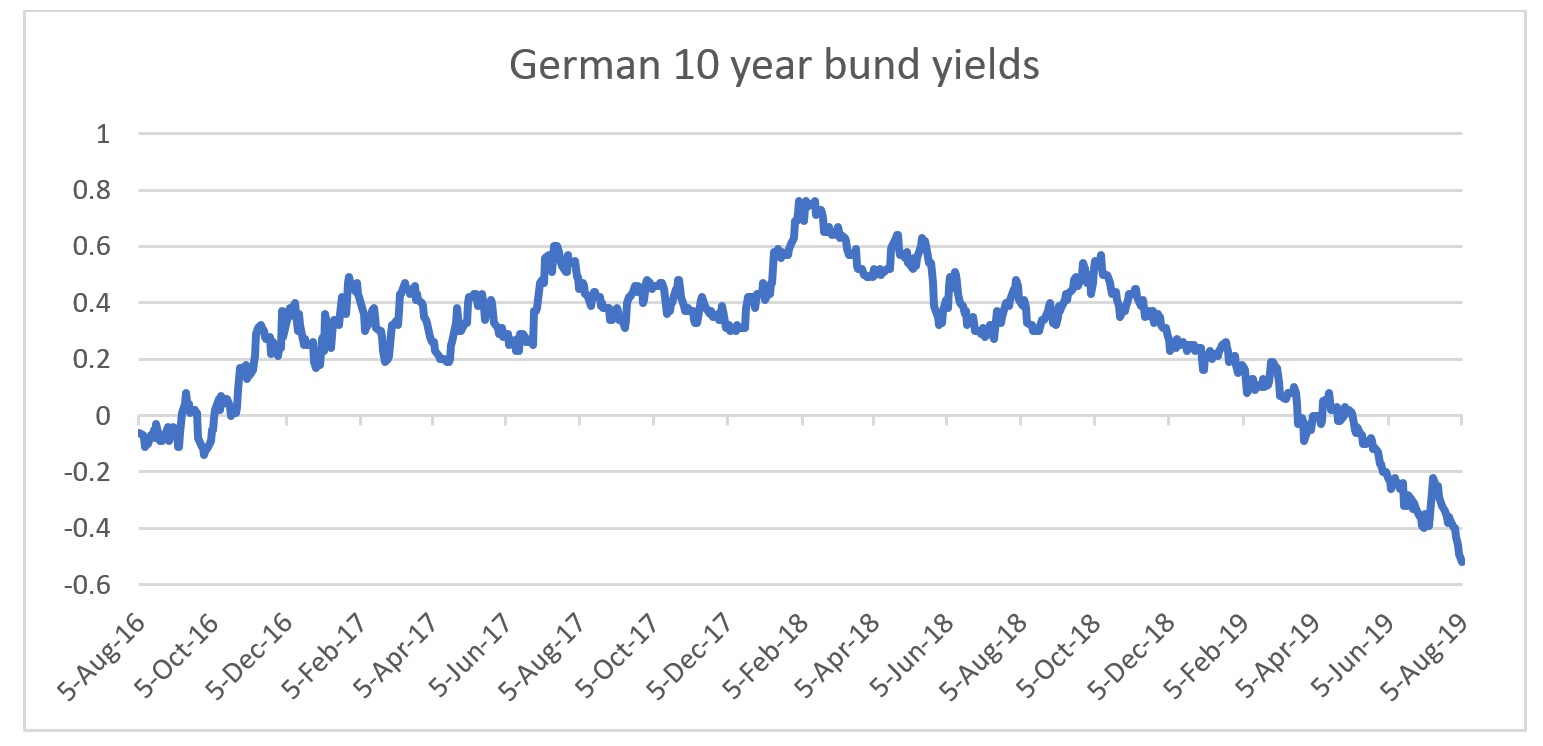

Meanwhile, the United States outperformed the rest of the world in 2017-18. But now, some of the boost from U.S. tax cuts is running out, and tax reform is already well priced into U.S. equity valuations. As a result, the 10-year Treasury yield, a measure of growth, has been signaling lower U.S. and global growth since it peaked in late 2018.

Lest you think the move lower in Treasury yields is happening in isolation, here’s a chart of 10-year German bund yields.

In other words, don’t listen to the left scream that tax cuts caused a slowdown, and don’t listen to the supply siders who say tax cuts would be working great, and would be causing greater capital expenditure, were it not for tariffs. Tariffs don’t help prolong the cycle, but America is highly insulated from global trade compared to the rest of the world, and the American consumer—most exposed to global trade—looks fine for now.

The credit cycle is the credit cycle, and a lot of it is now out of the control of the Fed, China, Trump, and tariffs. In fact, the epicenter of any global recession will likely be in Europe and China, not in America, although America does have a corporate debt bubble.

How This All Affects Politics

Trump is wagering that being the tough-on-China candidate will help him win reelection, and he’s probably right. His path to the presidency runs through the Rust Belt.

The de-industrialization of America has had terrible consequences for large pockets of the country, even if what we call free trade generally benefits a majority of Americans. An economist looks at people and thinks they are better off because they can buy cheap plastic toys at Walmart, even if they lost their factory jobs. Trump understands that people aren’t happy, and he (and a few other GOP politicians like Sen. Josh Hawley) understand that happiness is derived from a steady job and stable family life, not cheap imported goods. People aren’t math equations.

But further escalation in the trade war could dent the global economy. No president since World War II has won election on the back of a recession. In the United States, we could escape recession given our insolation from the global economy, however. What really matters is the change (in fancy lingo, the “delta”) of real disposable income growth and the unemployment rate.

The absolute level is less important. Even if the unemployment rate moves higher and stocks lower, as long as employment is increasing and stocks moving higher in the months before the election, Trump is set for a second term.

What can you do about all this? Stick close to your families. Live good and honest lives. And realize that in America, if things are to get better—measured not just by our economic circumstances but by our family and spiritual circumstances—our material wealth might have to get worse first.

The sandwich chain will start selling the product, made with Beyond Meat's plant-based protein, at 685 restaurants in the United States and Canada next month. The Beyond Meatball Marinara sub will be available for a limited time.

Several fast food chains are testing out menu items featuring meat substitutes to attract consumers who want to eat less meat for health or environmental reasons. Dunkin'(DNKN) recently announced that it is testing out a Beyond Meat sausage in Manhattan. Burger King will start serving a meatless version of its Whopper, featuring a patty made by Beyond competitor Impossible Foods, nationwide this week. White Castle, Carl's Jr., Tim Hortons, Qdoba and others also have meat substitutes on their menus.

For restaurants, testing out the products is a way to cash in on a fast-growing trend. US retail sales of plant-based foods have grown 11% in the past year, according to a July report from trade group Plant Based Foods Association and the Good Food Institute, a nonprofit that supports plant-based businesses. Barclays predicts the alternative meat sector could reach about $140 billion over the next decade, capturing about 10% of the global meat industry.

Most restaurants are chasing flexitarian eaters rather than strict vegans. Subway's Beyond sub, for example, comes with Parmesan cheese.

Beyond(BYND) and Subway worked together to develop the Beyond Meatball, which is only available at Subway restaurants.

Both Beyond(BYND) and Impossible have seen demand for their products surge. Beyond's revenues reached $67.3 million in the second quarter, up from $17.4 million during the same period last year, a 287% spike.

And demand for Impossible's product has grown so much that the company had a shortage earlier this year. Last week, Impossible announced a partnership with meat processor OSI to expand its production capacity. Impossible is private and doesn't share its sales figures publicly.

When the United States declared China a currency manipulator on Monday, long-building trade tensions between the world’s two largest economies spread to the combustible realm of currencies — with potentially huge consequences for the global financial system should the escalation continue.

Did China allow the value of the yuan to fall against the dollar simply to allow it to better match the nation’s economic situation, as the country’s leaders and many international economists argue? Or was it, as President Trump contends, an effort to give Chinese exporters an unfair advantage in trade?

That clash reflects Mr. Trump’s rejection of the consensus of global economic policymakers. That consensus says countries should be free to set monetary policies aimed at generating sustained growth, even if that causes their currency to depreciate. And they should be free to manage their exchange rates so long as they keep those rates broadly in line with their economic fundamentals.

The conflict also reflects the president’s singular focus on reducing trade deficits, which he has argued make the United States a loser in the global trade system. But waging a currency war could come at a big cost.

“I worry it further undermines the international framework that has supported decades of faster growth,” said Kristin Forbes, an economist at M.I.T. and a former official of the U.S. Treasury and the Bank of England. “Exchange rates are the shock absorber in the global economy.”

There have been international strains over currency valuations for years, all the more so in a world in which all the major economies are coping with sluggish growth. But the newest currency frictions are different.

Up until now, countries have been focused on stimulating their domestic economies. In particular, central banks have cut interest rates and taken other steps to pump money into their financial systems. That tends to lower the value of their currency. After all, investing in a currency with lower interest rates is less attractive, all else equal, than in one with higher rates.

But the conventional wisdom among international economists is that this doesn’t count as currency manipulation. It’s not a game in which one country’s win means another must lose. Lower interest rates should generate more economic activity, which makes the whole world better off.

The Trump administration has introduced a zero-sum approach to global currency policy — envisioning a loser for every winner — that violates the spirit of those rules.

In that sense, the latest moves risk upsetting a relatively stable order, creating unpredictable ripple effects. When currencies swing wildly, they can pull along the economies of some of the most powerful nations, such as by crushing entire sectors of the economy that find themselves uncompetitive after a swing in global exchange rates.

And it could undermine the central role the United States has played in the international financial system, especially if the accusations of manipulation are followed up with concrete retaliation to try to artificially depress the value of the dollar.

“The dollar being the primary global currency has enormous benefits for the U.S., but with the side effect that when the U.S. tries to depreciate, there are limits on how much it can do that,” said Adam Posen, president of the Peterson Institute for International Economics. “But if the U.S. abuses its privilege too much by bullying, there will eventually be a switch.”

The decision to name China a currency manipulator does not, in and of itself, do much. But it could be followed up with pressure on the International Monetary Fund and other nations to make similar findings and lean on the Chinese to adjust their policies. Or it could lead to direct intervention in foreign exchange markets by the United States Treasury.

This is not the first time President Trump has accused a major trading partner of using currency policy to mistreat the United States.

He assailed the European Central Bank for moving toward monetary stimulus in June — complaining on Twitter that the resulting drop in the value of the euro was “making it unfairly easier for them to compete against the USA.”

The European Central Bank explained its stimulus as an effort to keep Europe from sliding back into recession. When the central bank first undertook its “quantitative easing” policies, it was with encouragement from the Obama administration, which believed a stronger European economy was ultimately good for the U.S. economy, despite its effect on currencies.

Similarly, the Trump administration’s decision Monday to name China a currency manipulator — for allowing the value of its currency to fall — does not align with how mainstream economists view China’s move.

With the economy slowing in China, in part because of the trade wars, market forces tend to push its currency lower. But the People’s Bank of China has defended the currency from big drops, aiming to prevent capital from flowing out of the country or destabilizing the world economy.

The “manipulation” that took place Monday morning wasn’t artificially depressing the Chinese currency to seize advantage with trade partners, but engaging in less manipulation in order to allow it to fall closer to its market-determined rate.

There is a more nuanced case to be made against Chinese currency policy — that it did intervene for years to push down the value of its currency, ending in the early 2010s, and that Chinese economic might was built on an unfair practice. But the Trump administration’s announcement focuses on the more recent actions, in which different economic rationales apply.

There is also a paradox for President Trump. Because of the dollar’s unique role as the global reserve currency, when panic sets in overseas, money tends to flow into United States Treasury bonds, which are viewed as the safest assets on earth. But that movement tends to prop up the value of the dollar and push overseas currencies lower.

In other words, the more chaos he injects into the global economy by trying to pressure China, Europe and others to depreciate their currencies, the more upward pressure there will be on the dollar, undermining those efforts.

That is potentially the worst of both worlds. When the dollar rises on currency markets because the United States economy is booming, it may be hard on American export industries, but at least it takes place in the context of strong growth.

But for the dollar to surge because of a global economic troubles, it means exporters suffer at the same time that the overall economy is under pressure. A particularly extreme example of this happened in the fall of 2008, when the United States economy was in free fall and yet the dollar rose because of the global financial crisis.

A habit of the Trump administration has been to link seemingly unrelated items in its dealings with other countries — using tariff threats to try to influence Mexican immigration policy, for example.

If the Trump administration continues down the path of using currency policy to try to bludgeon China over trade, technology and national security issues, it will signal a remarkable expansion into a policy area that has been a source of stability in recent decades.

“It’s dangerous to start a currency war because you don’t know where it will end,” said Eric Winograd, chief U.S. economist at AllianceBernstein. “We’ve seen with the trade war that it started in one place, and ended up much broader. There’s every risk a currency war will do the same.”